Contact Us

Let’s Partner for Your Next Big Presentation

Consult with our Business Advisor

.webp)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Many founders miss the distinction between rejection and forgetting. An investor's decision to reject a pitch implies that they've considered it and found it wanting. An investor's failure to consider a pitch implies they haven't recalled anything worth considering about it.

An investor can go through eight meetings in a single day. They will remember two of them clearly. The other six, though, live on only in vague impressions about the logistics, fintech, and copious slide decks. The founders who conducted the other six meetings feel rejected; in reality, they never had a chance.

Designing a memorable deck is a solution to the problem of forgetting. It is focused on retention, not persuasion. Because one cannot persuade a person who has forgotten what one said. A compelling pitch deck doesn’t just inform; it creates a mental model the investor can reconstruct hours after the meeting. This is why thoughtful investor presentation design is as strategic as it is visual.

The founders' perception of clutter is based on quantity. Many believe a slide deck with excessive slides, or a slide with too much text. But what clutter really is is something else.

The definition of clutter is any content within a slide that does not directly support the single argument made on that slide.

A slide with three bullet points may be clutter if two of them need to be placed in another slide. A slide with a single picture may be clutter if it is unnecessary to the claim. A slide with projections may be clutter if there is no clear claim at the top explaining what conclusions investors must draw from the numbers.

Clutter is not about volume, it's about intention. With regard to every element on every slide, the designer needs to ask: Is this supporting the argument of this particular slide?

This list isn’t about design. These are structural and strategic decisions made before designing, deciding if the investor will leave remembering your thesis or carrying vague impressions of the pile of slides.

The most common characteristic of the messy slides is always the same question – what is the main point I want my investor to believe after reading this slide? If the answer takes more than one sentence to formulate, there are more ideas than one on this slide.

It seems self-explanatory, yet very few founders do it right. Startups build slides like writing an argumentative paper - by piling up all evidence. There are five functions in a product slide. In the market slide, there is a TAM, SAM, SOM, and growth rate. Team slide includes every qualification of each team member. All statements may be absolutely true. However, put together, they create a mess that investors scan and forget instantly.

The discipline doesn't mean deleting any data. It means finding a unique key statement for each slide and moving everything else to another slide or an appendix. Once you have one statement to dominate a slide, you get a memorable slide. And if memorable statements stack up, they become your thesis. The thesis is what you take out of the room with you.

The test: Cover your slide with your hand. Formulate the one idea you would like the investor to take away from reading it. If it takes more than one sentence to explain it – your slide is still unfinished.

The typical structure of the slides used to be academic. You start with evidence and finish with conclusions. For peer review, it is the perfect method, yet it makes no sense for a pitch when an investor needs to decide if your thesis makes sense.

Once your presentation starts with three bullets of evidence and concludes with something important in the fourth bullet at the end of the slide, the investor has to remember all three pieces of evidence until they see the conclusion. They don't do it often. Forming conclusions after a brief glance at the first bullet, investors are distracted by the time you get to making conclusions.

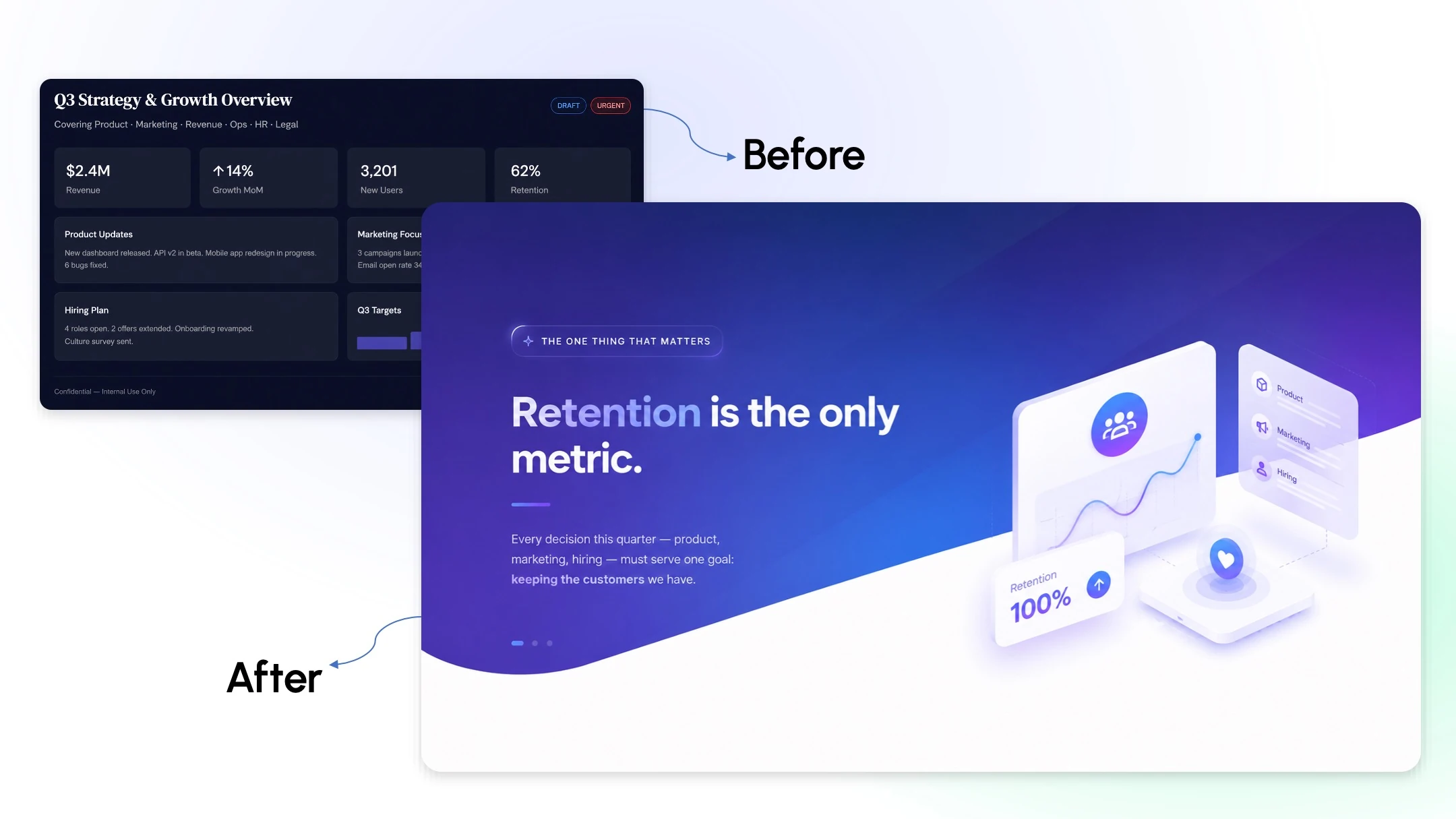

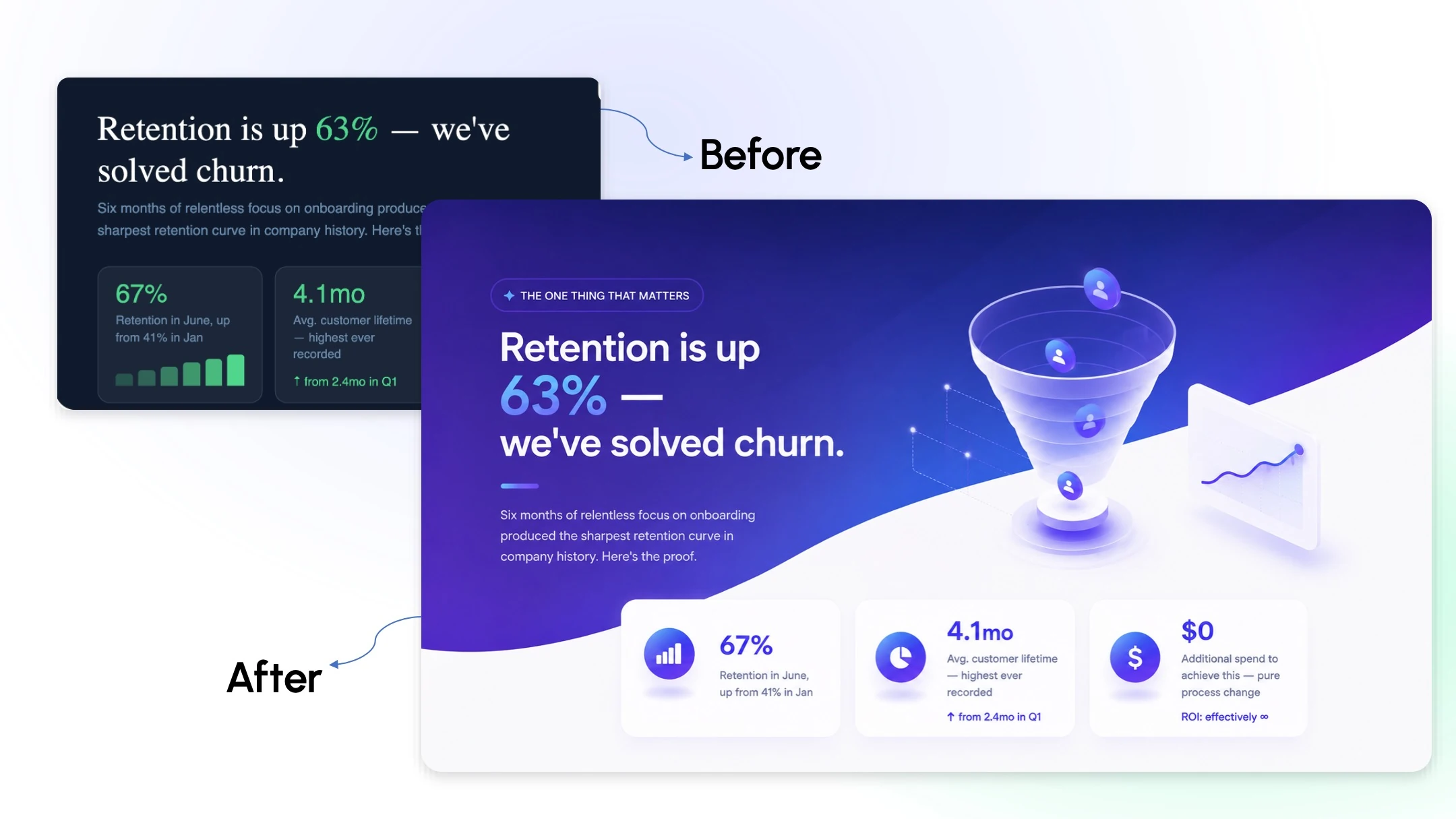

To solve the problem, you just need to reverse the order of statements. Put your claim on top of the slide, then back it up. Not "340% revenue growth, fueled by enterprise sales, with retention over 90%" in the footnote of the chart, but rather "enterprise retention is the engine" as a slide headline, and the chart serves as proof. The investor reads your headline, sees the chart, and gets convinced.

The test: Read only slide headlines in succession. Do they tell you a coherent story on their own? If they don't – the headlines are just labels, not claims.

All great pitch decks have a center of gravity – one key insight about the market, timing, or business, to which everything else ties back. It's not the mission statement. It's not the product description. It is one insight that, once an investor gets it, makes all other slides make sense.

For a logistics start-up INK PPT worked with, the core insight was not "last-mile delivery is broken." It was the simple observation that the misrouting costs go up in non-linear fashion beyond a certain network density and no one had ever built a platform around it. Once an investor got this idea, the rest became obvious. It explained the product, market size, and positioning. The insight did the job of persuasion; the rest of the deck provided the proof. The founder knew it, but it never made it into the deck until we found out about it.

The test: When investors remember only one thing about your deck, what should that be? Can you put this one sentence onto one slide?

A presentation design agency designing branded templates to your deck has done half the job. The other half is crafting slides in such way that the visuals help tell the story, not just reinforce branding. Founders who invest in pitch deck and presentation design together — not just one or the other — consistently build decks that are both visually coherent and structurally persuasive.

It means that the most important sentence on each slide is the biggest and most contrasting one. It means that charts get annotated with the takeaway, not just the numbers. It means that the slide telling an argument about the simplicity uses a minimalist layout, while the slide talking about the scale gives off a feeling of scale.

INK PPT worked with an enterprise software company whose solution deck told the audience that their platform reduces operational complexity. The slide with this statement was filled with seven bullet points, two call-out boxes, and a process map that consisted of nine nodes. The visuals said the exact opposite of what the slide claimed. No one would remember this claim because the visuals contradicted the argument from the very first moment. A redesign wasn't the solution – the problem could be fixed within a single slide, in one sentence and with one three-step diagram.

The test: Identify whether each slide uses the visuals to reinforce the argument or leaves investors indifferent. The latter is wasted potential; the former creates a credibility problem.

Data in a deck becomes powerful only after investors have developed an interest in it. To an entrepreneur this seems wrong – isn't the data what sparks investors' interest? On the contrary, data only adds power to the storyline that generates an interest.

Opening a deck with traction data before the problem and the solution is like dropping a number into a vacuum. An investor sees 22% growth per month, without knowing what kind of number to expect, whether it is impressive and sustainable in this context.

Telling the problem first and proving the solution with traction data at the end of the deck is like putting a period at the end of the sentence. Once an investor begins to understand why your solution works and is better than others, 22% growth is nothing more than a confirmation of an argument they were making themselves.

The test: Identify the narrative required before introducing data in your deck. If the narrative follows or is missing entirely, the numbers speak louder than the story.

The last slide in most pitch decks is a "Thank You" slide with the team's contact information. This is a mistake. Or sometimes, it's a recap of previous points that the team thinks are important. This too is a waste. When a potential investor leaves a room, their final impression of that meeting depends entirely on the final slide that they saw.

A good closing slide makes one decision clear and time-sensitive. It is not: "We are raising 10 crore" + contact information. A good closing slide reads something like: "We are closing this funding round in eight weeks; there are two spots left at the current terms, and this exact milestone is what this capital will help us achieve." Investors are not being asked if they want to fund a business – rather, investors are being asked if they wish to take a stake by a certain date.

This framing is not coercive – it is simply clear. Investors make quicker decisions when there is structure around a particular choice. A deck that ends without clear decision-making will leave that choice up to the investor, who will usually decide not to make any more effort to engage in further conversation.

The Test: Go back to the last slide of your pitch deck. Is this slide defining clearly what decision investors must make, the timeline, and what will be lost by delay? If not, then this closing slide is weak.

This is a case study of a pitch process in which the above six criteria have been applied to a pitch deck that had high quality material and content but had trouble advancing conversations with investors.

Persuasion is dependent on conscious logic processing. Stickiness has to do with the limitations of working memory and cognitive structures. They are two very different things, and while much pitch-deck advice focuses on the former, little attention is paid to the latter. A pitch-deck that articulates six arguments is harder to remember than a pitch-deck that makes a single central argument, backed by five pieces of evidence. The former requires the listener to keep six distinct strands of thoughts in their mind and synthesize them together into an idea; the latter requires only one strand of thought with five pieces of evidence backing it.

Even if an investor is persuaded at the end of a multi-point pitch deck, this does not mean they will remember any of it. Come Thursday evening, investors are likely to encounter three additional pitches. By Friday morning, all six arguments will melt away in their head into some vague notion that this pitch might have been interesting. This is not a storytelling issue – this is a structural problem. Even the most compelling stories get lost to cognitive overload. This is why every compelling pitch deck must be built around a single retrievable argument, not a checklist of business facts.

Complete the following six tests on your current deck before your next investor meeting.

1. Single job test: Can you summarize in one sentence what each slide is asking the investor to believe? If any slide needs two sentences, it has two jobs.

2. Argument test: Reading only the headlines in order, is there a clear story being told? If they are just labels and not arguments, then this is evidence and no case.

Insight test: Is there one slide in this deck that, if the investor remembered nothing else, captures the essential point? If it takes you longer than three seconds to figure it out, then it doesn’t exist.

3. Visually dominant test: Does the design highlight the most important argument by making it visually dominant? If it’s design that looks great but argues poorly, it’s failed.

3. Story test: For each piece of data, was the story already told that gives meaning to the number? If the investor sees traction before understanding the problem and the solution, then the data doesn’t have context.

4. Conversion test: Does the ending slide show the investor exactly what they’re deciding, when, and what the capital gets them to? If not, then it’s polite but won’t convert.

Any one of these tests that fails will stall investor discussions. And the fix isn’t cosmetic; it’s an architectural problem. Start with your deck’s architecture, not with your design brief.

If a founder builds a pitch deck and then fails to land their investment despite having exited twelve meetings with twelve generic “we’ll be in touch” replies, then they haven’t been rejected. They’ve simply been forgotten. The former problem can be solved. But it requires a different diagnosis than the latter.

On the other hand, founders who manage to clear away all unnecessary slides without losing their clarity cutting slides not because the meeting ended, but because the deletion improves their pitch are those who enter investor meetings prepared to answer one thing and only one thing: what must the investor know to take a leap? This confidence comes from having built their entire pitch deck for that purpose.

That’s what makes a pitch deck sticky, not the design, not the slide count, not even the underlying business. It’s the architecture and the discipline to eliminate everything that doesn’t advance that argument.

As a passionate explorer, I see crafting the perfect story as embarking on a refreshing Himalayan journey. Every narrative is an adventure, a voyage of imagination, meticulously molded into captivating presentations. I'm here to guide you, ensuring your story becomes an unforgettable odyssey, with each creation as a vibrant landscape ready to captivate eager audiences.

About the Author

Consult with our Business Advisor